Retail Margin Pressure 2026: Why Reactive Discounting Is Making the Squeeze Worse

The 2026 edition of McKinsey's State of Grocery Retail Europe landed this week with a single number that every retail CEO should screenshot: for the third consecutive year, cost and margin pressure tops the priority list. Not digital. Not AI. Not sustainability. Margin. (McKinsey, via ESM Magazine)

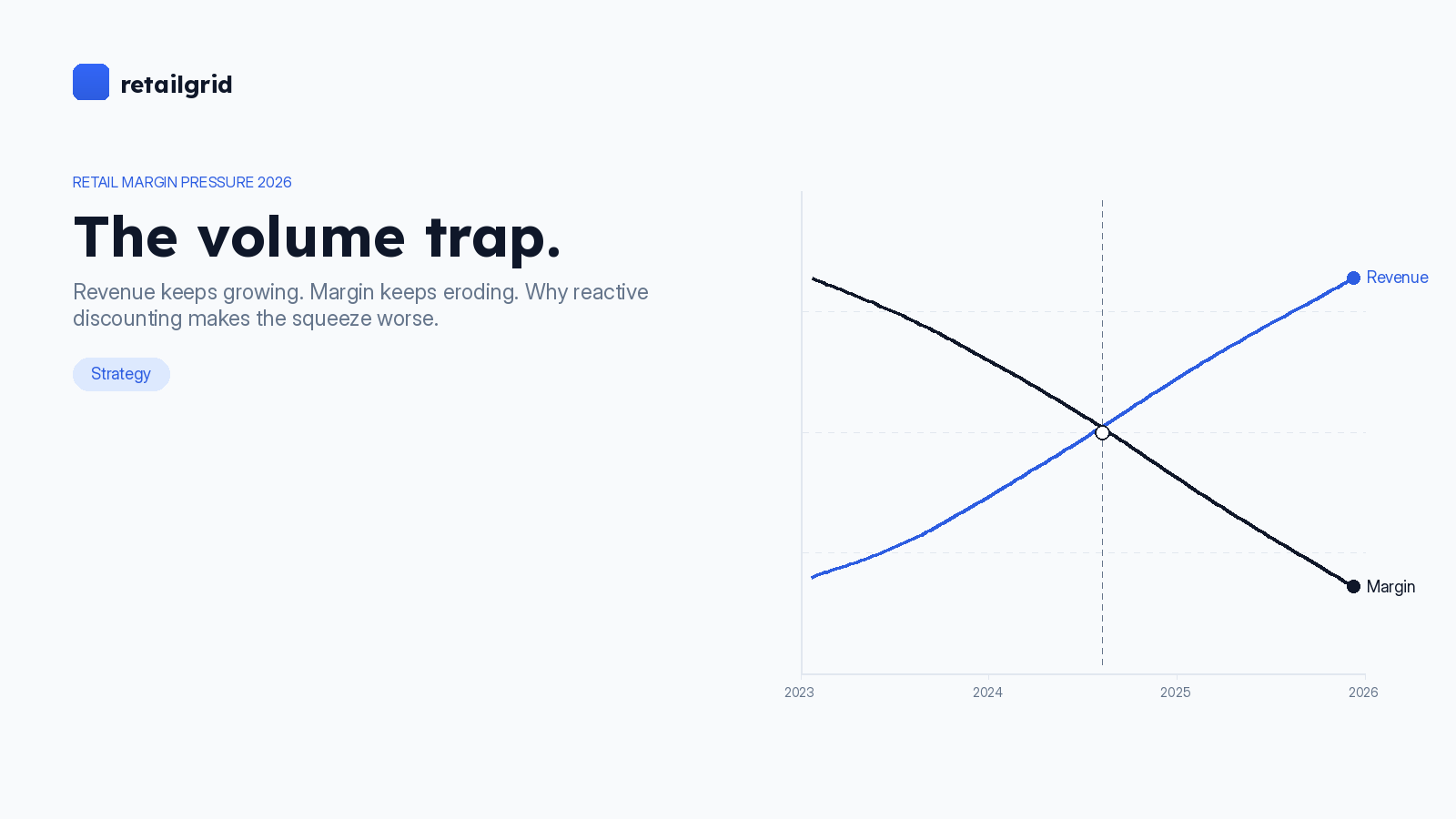

The same week, REWE Group crossed the €100 billion revenue threshold — and quietly disclosed that its operating profit declined. (ESM Magazine) Volume up, margin down. If that pattern sounds familiar, it should. It is showing up in every boardroom from Helsinki to Madrid, and it is the defining retail story of 2026.

Here's the uncomfortable part: most of the playbooks being used to fight it are making it worse.

Retail margin pressure 2026: the three-year trap

The squeeze didn't appear overnight. It arrived in three overlapping waves, and each one left behavioral scar tissue.

The first wave (2023) was the inflation shock. Input costs jumped, retailers pushed prices up, consumers absorbed it because they had no choice, and the P&Ls actually looked fine — revenue was inflating faster than cost.

The second wave (2024–2025) was the elasticity correction. Consumers traded down, switched to private label, and got disciplined about baskets. McKinsey's 2025 consumer survey found 84% of shoppers said they'd stick with private label even if their spending power recovered. (McKinsey) That's not a cyclical shift — that's a new baseline.

The third wave (2026) is the margin one. Volume growth is anemic, input costs are sticky, and retailers can no longer pass increases through because consumers are price-sensitive and competitors are watching every shelf. McKinsey is explicit: "grocers may not be able to fully offset growing sourcing costs by increasing consumer prices due to high price sensitivity and competitive pressures." (McKinsey)

The playbook retailers reach for — deeper promos, broader markdowns, louder price communication — was built for wave one, when passing cost through worked. In wave three, it accelerates margin erosion. You are effectively discounting to win share you already had.

What the data actually says about the winners

The most striking finding in the 2026 report is not about promo depth or AI or private label share in aggregate. It's about who is gaining share.

Retailers with above-average private label share had a 2.8× greater likelihood of gaining market share than their peers over the past six years. (EuroCommerce) That is not a small edge. That is a structural advantage.

But — and this is where most of the commentary misses the point — private label is no longer winning on price. McKinsey is specific: "Private label no longer competes with branded goods on price. Its growth is driven by the diversity of assortment offered, including budget, premium, free-from, organic, local, or other forms of innovation."

Read that sentence twice. The retailers pulling ahead are the ones who treat their own-brand shelf as a product-design problem, not a pricing problem. They know which tiers should play which roles. They know which SKUs are there to build trust, which are there to protect margin, and which are there to express a point of view.

That is a pricing and assortment decision — made structurally, at the category level, and re-made every season. It is not a spreadsheet exercise and it is not a one-time project.

Why reactive pricing makes the squeeze worse

Here is a pattern we see repeatedly in mid-market retailers (€10M–€500M revenue, 10k–200k SKUs): when margin pressure hits, the first reflex is tactical.

Run more promos. Match competitors faster. Extend the flyer. Add a third "everyday low price" lane.

This feels decisive. It is also quietly catastrophic.

Every tactical price cut ships a message down the chain. The category manager sees margin fall and asks for a cost concession. The supplier grants it — but only by reducing quality, changing pack size, or pulling marketing support. The shopper experiences a worse product at a lower price. The brand positioning drifts. The next season starts from a weaker baseline.

Meanwhile, none of the actual pricing questions have been answered:

- Which SKUs in this category should be price-competitive, and how competitive?

- Which SKUs are being bought primarily on trust, not price?

- Which promotions are stealing volume from the next week versus generating real incremental demand?

- Which private label tiers are under-indexed relative to shopper demand?

You can't answer those questions with a markdown calendar. You answer them with a structured, repeatable pricing process — one that assigns every SKU a role, measures elasticity at the level where it actually varies, and decides promo depth based on what the math says rather than what competitors did last week.

What "structured pricing" actually means

The phrase "structured pricing" gets used loosely. Here's a concrete definition:

1. Every SKU has a role. Key-value items (KVI), traffic drivers, margin builders, signature items, tail. Roles are assigned deliberately, reviewed each season, and baked into pricing and assortment rules.

2. Pricing rules are explainable. Not "the algorithm said so." A category manager can describe — in one sentence — why a specific SKU moved from €4.99 to €5.19, and what signal triggered it.

3. Competitor prices inform, don't dictate. Matching every competitor move on every SKU is how you concede control of your P&L. A structured process distinguishes "we must match" (a small subset) from "we should watch" (most of the shelf).

4. Promotions are measured against what would have happened anyway. Not against last year's same week. Real incremental lift, net of cannibalization and pull-forward.

5. The pricing process runs every week, not every quarter. Retail moves too fast for quarterly reviews. But it also doesn't need real-time; most of the gain is captured by a disciplined weekly cadence.

None of this requires an enterprise-grade transformation. It requires structure, clean data, and a tool that lets a pricing manager see the decisions, not just the outputs.

Where mid-market retailers keep getting this wrong

The common failure modes, in order of frequency:

- Spreadsheets as the system of record. Pricing logic lives across a dozen tabs that nobody owns, no version history, no audit trail. It works at 5,000 SKUs. It breaks somewhere between 10k and 20k.

- Black-box AI as the replacement. The pendulum swings hard. A tool ingests data, emits prices, the team can't explain why, the category manager overrides half of them, and trust erodes fast.

- Competitor-matching as strategy. It isn't. It's a tactic — useful on maybe 5–15% of the assortment. Used on 100%, it is a slow way to give away margin.

- Promos as the only lever. If the answer to every margin question is "run a promo," you don't have a pricing strategy. You have a discount schedule.

- No SKU role framework. Which means pricing decisions happen item-by-item, with no system view. Category managers make locally rational choices that add up to portfolio chaos.

[Editor: add inline visual — A visualization showing two retailer trajectories on revenue-vs-operating-margin axes over 2023-2026 — one with flat margin as revenue grows (the "volume trap") and one with margin expansion (the "structured pricing" path). Label the divergence point as "wave three / 2026."]

What this doesn't change

It's worth stating plainly: structured pricing doesn't rescue a business model that isn't working. If a retailer has the wrong store footprint, the wrong private label quality, or a supply chain that can't deliver on the assortment promise, better pricing won't fix it.

It also doesn't replace judgment. The best pricing teams we see use structured tools to extend the reach of their category managers — not to replace them. The tool handles the 80% of decisions that are mechanical so the humans can think hard about the 20% that actually matter.

And it isn't a quarter-long project. A mid-market retailer can have role-based SKU segmentation, weekly rule-based repricing, and cleaner promo measurement running inside a single season. The constraint is not technology. It is organizational willingness to stop treating pricing as a reaction and start treating it as a decision.

The CEO question for Q3 2026

Every CEO of a mid-market retailer will face a version of the same question this summer: margin is down, volume is flat, the board wants a plan. The tactical answer is always available — run more promos, cut SKUs, push the supplier. It will move the P&L for a quarter. It will leave the structural problem untouched.

The better question is this: if we opened up our pricing process and looked at the last 90 days of decisions, could we explain, SKU by SKU, why each price is what it is? And could we predict — within a reasonable band — what would happen if we changed it?

If the answer is no, you don't have a margin problem. You have a pricing-decision-making problem. The margin issue is the symptom.

The third year of margin pressure isn't the worst news in the 2026 report. The worst news is that the retailers who figured this out five years ago now have a 2.8× edge on everyone else — and the gap is widening.

Retailgrid helps mid-market retailers run structured, explainable pricing decisions at 10k–200k SKU scale — Excel-feel, big-data power. If this mirrors the pricing week you're running, we'd like to hear from you. Tell us how you price today.