Build With AI, or Buy From People Who Build With AI? Retail's 2026 Build-vs-Buy Reset

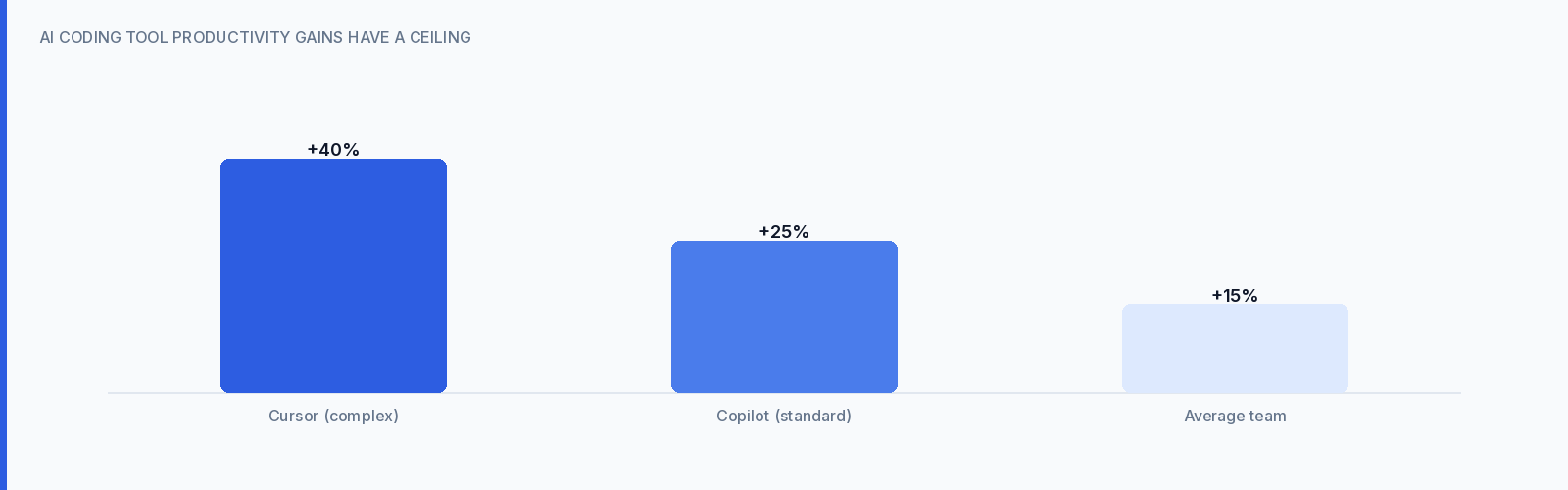

By January 2026, 74% of developers worldwide had adopted AI coding tools at work. Microsoft and Accenture published internal studies showing 26% productivity gains, with Cursor users reporting 35–45% faster feature completion on complex tasks. In the retail tech conversations we have every week, the implication shows up the same way: "With AI, why would we buy this when we could build it ourselves in a quarter?"

It's a fair question. It's also the wrong frame.

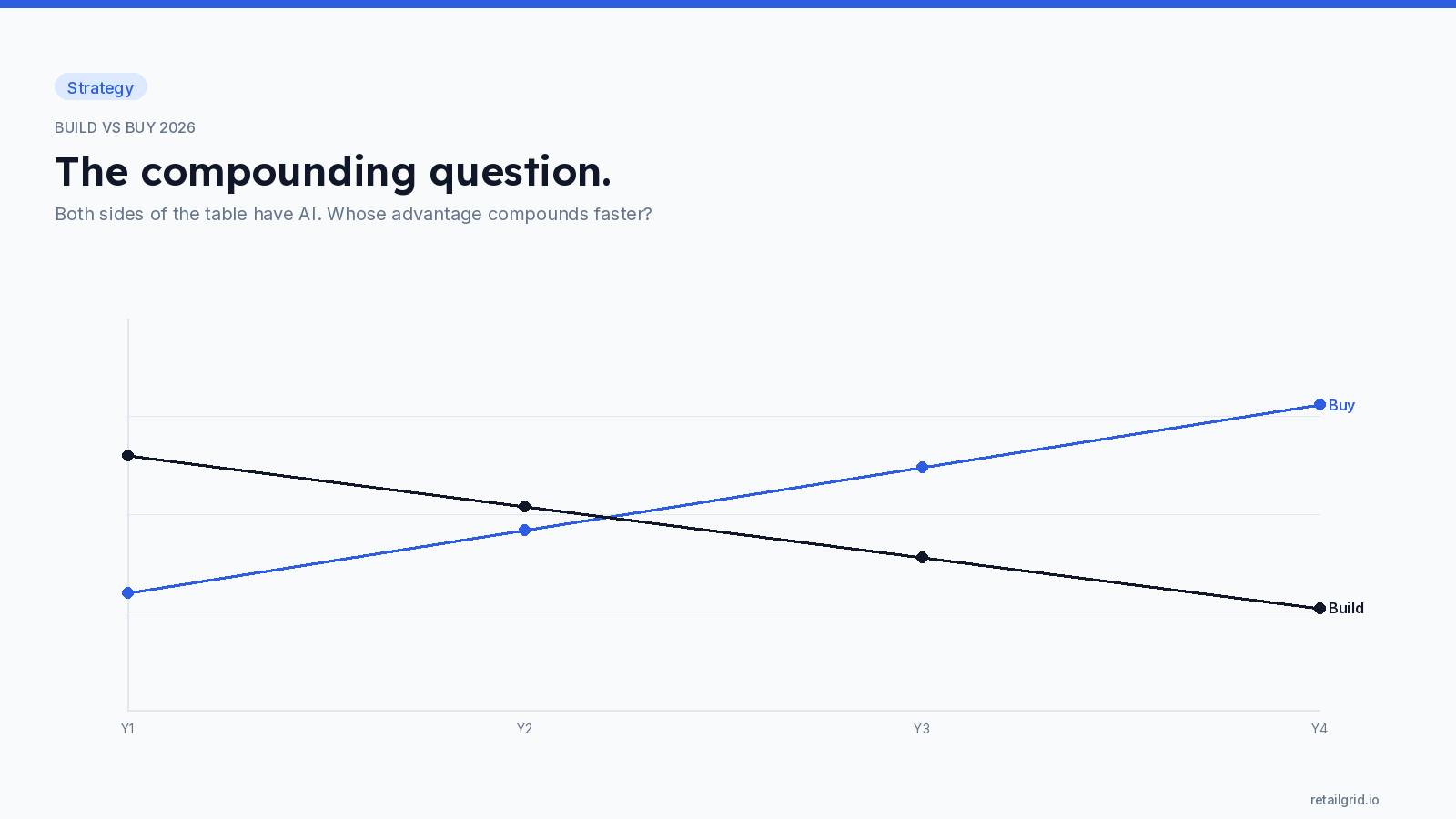

The old build-vs-buy dilemma assumed AI was on one side of the table — yours, if you decided to build. In 2026 the AI advantage exists on both sides. The vendors you'd be buying from are themselves shipping faster, cheaper, and more responsively because they build with AI too. The retail leaders making this call well aren't asking "should we build or buy"; they're asking "do we want our AI leverage applied to one company's workflows, or to a vendor's whole customer base?"

This is the C-level reset on build-vs-buy.

What Changed in the Build Column

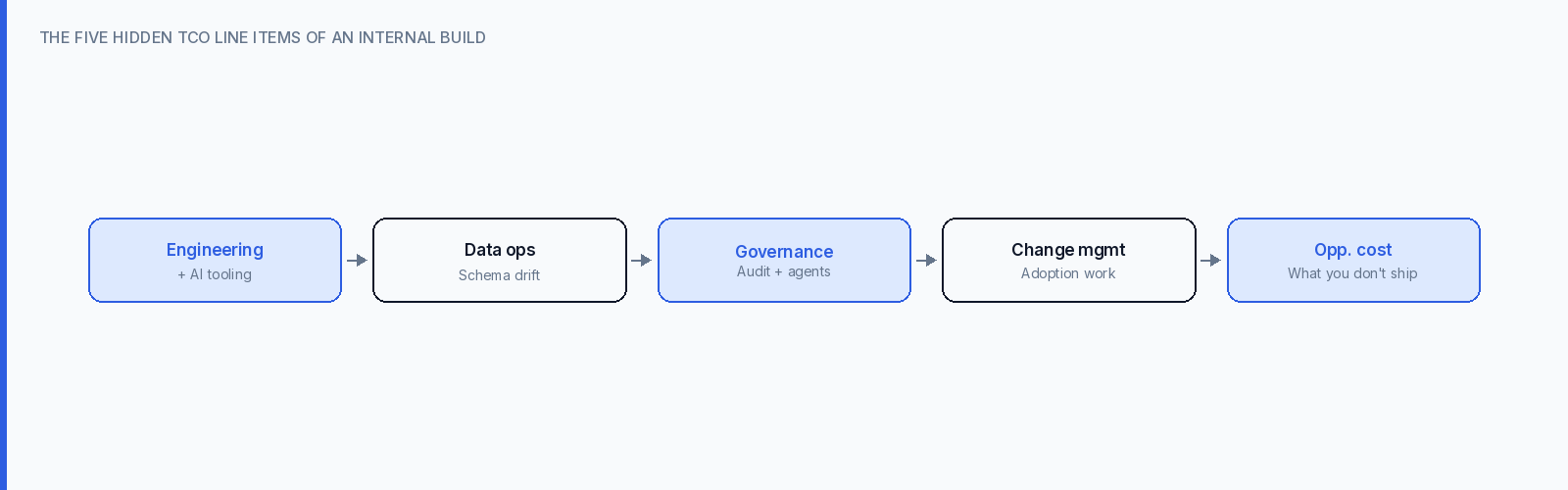

The build case has never looked stronger on paper. AI coding tools have collapsed three of the four traditional cost lines

The fourth cost line — running the thing in production — did not move. And that is where the math actually plays out.

McKinsey research found 66% of enterprise software projects exceed budget, with every additional project year increasing cost overruns by 15%. The Software Improvement Group's analysis of enterprise TCO points at the same blind spot from the other direction: maintenance and "keep the lights on" work accounts for around 70% of total cost of ownership, with technical debt eating roughly 30% of that. AI sped up the front of the production pipeline. It did not shrink the back.

For a mid-market retailer, that back end includes data engineering against ERPs that change schemas without notice, integrations with point-of-sale and e-commerce platforms that update on different release cycles, on-call rotations for a pricing system that decides the gross margin on tomorrow's promotions, audit trails for SOX-relevant decisions, and the change-management work to retire whatever spreadsheet the new tool replaces. None of that is harder or easier because of AI. It still has to be staffed.

What Changed in the Buy Column

The mistake in most "let's just build it" conversations is comparing 2026's build economics against 2022's vendor economics.

The vendor side moved too. AI-native software companies are shipping at a velocity their pre-AI predecessors couldn't match. The same productivity uplift that makes your engineers faster makes your vendor's roadmap faster. A category that used to see a meaningful product release every twelve to eighteen months now sees one every quarter. Pricing models have shifted alongside — outcome-based and consumption-based pricing have moved from the edges into the mainstream, because vendors with AI cost leverage can underwrite the risk of being paid for results.

A16z's survey of 100 enterprise CIOs showed the buy side reasserting itself through 2025 and into 2026 specifically because of how fast AI-native vendors moved. Off-the-shelf solutions are eclipsing custom builds in categories that even two years ago looked like obvious internal projects — for customer support, over 90% of enterprises are now testing third-party AI rather than building.

The vendor-buy decision in 2026 is less "we don't want to build that" and more "the vendor will out-iterate our internal team because they have a thousand customers' worth of feedback compounding into their roadmap, and they have AI leverage applied across all of it."

The Total Cost of Running Something in Production

Most retail finance teams scoping a build use a model that looks something like this: development cost in year one, smaller maintenance cost in years two and three. AI shrunk the first number. The second number is the one that decides whether the project succeeds or quietly becomes the next legacy system.

A defensible 2026 TCO model for a retail-pricing-grade internal build needs five lines:

When that model is run honestly, the build case usually wins for capabilities that are core differentiators and loses for capabilities that are table stakes hygiene. The category mistake of 2026 is treating retail pricing — which is hygiene for some retailers and a differentiator for others — as if it were one or the other for everyone.

When Build Still Wins

Three conditions, and they have to be true together.

A genuine differentiator, not a hygiene capability. If your pricing approach is the same shape as your competitors' — KVI lists, competitor matching, margin floors, promotion calendars — that is hygiene. Hygiene loses to vendors. If your pricing approach is genuinely unusual — say, a sub-category-level demand model that depends on first-party loyalty data nobody else has access to — that is differentiator territory. Build there, but only there.

An engineering organization with platform leverage. Building one internal tool is a project. Maintaining one internal tool indefinitely is a team. Maintaining ten over five years is a department. If your existing engineering org does not already operate a platform on which the new tool can land, the tenth year of TCO will be brutal.

Data the vendor literally cannot replicate. Multi-tenant vendors have an advantage your internal build cannot match: they see hundreds of retailers' data and can train on patterns yours alone won't surface. The build case has to override that with first-party data the vendor cannot ever have. If you can't articulate what that data is, the build case is weaker than it looks.

When Buy Wins Decisively

The mirror image. Buy is the right answer when:

The New Questions to Ask

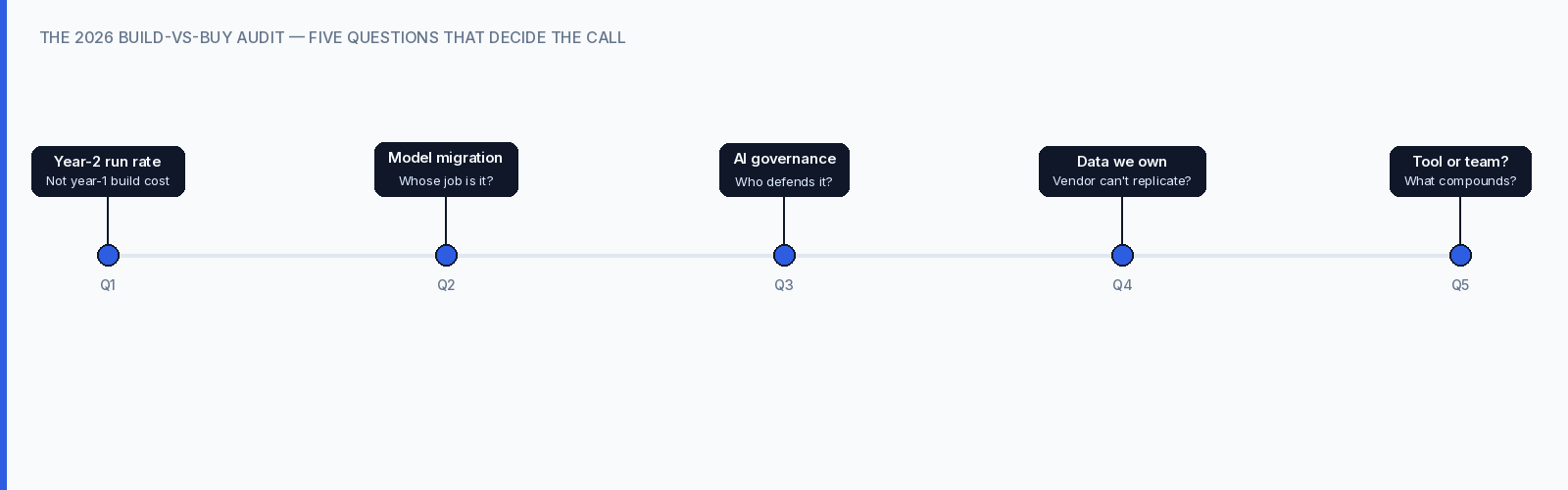

Build-vs-buy decisions used to come down to a spreadsheet. In 2026 it is closer to a five-question audit. If your team cannot answer all five with conviction, the answer is buy.

1. What's the second-year run rate, not the first-year build cost? AI made year one cheap. Years two through five tell the truth.

2. How fast does the underlying model layer shift, and who is responsible for following it? The frontier model you build against this quarter will be deprecated within twelve to eighteen months. Whose job is it to migrate the agent, re-validate the prompts, re-run the eval suite, and roll back if the new model regresses? Vendors do this for a living. Internal teams treat it as project work.

3. What is our governance story for an AI agent making decisions in production? Deloitte's 2026 State of AI in the Enterprise survey ranked data privacy and security at 73% and governance capabilities at 46% as the top concerns of 3,200+ leaders. Building an AI tool is one decision. Defending it to your auditor is another.

4. Do we have the data to make our build better than the vendor's? Be specific. Not "we have a lot of data." What signal does your internal build have access to that a multi-tenant vendor can't ever have? If you cannot name it in one sentence, you don't have it.

5. Are we buying a tool, or are we buying the team that builds with AI? This is the reframe that changes most decisions. The "buy" option in 2026 is not just software. It is the vendor's engineering org, their AI tooling, their model migration discipline, their roadmap velocity — applied to your problem, on your timeline, paid for at the marginal cost of whichever customer they serve next. That is what compounds.

What This Doesn't Change

A few things AI didn't fix and probably won't.

You still need clean data. The retailers who fail at both build and buy in 2026 fail at the same thing: dirty product hierarchies, inconsistent SKU mappings, sales records that don't reconcile to ledger. AI on top of bad data is faster bad decisions. Whichever path you choose, the data work is yours to do.

You still need an executive sponsor. The internal build that fails is rarely a coding failure — it's an adoption failure that traces back to no senior accountability for the change. The vendor implementation that fails is usually the same shape. AI did not change organizational physics.

And you still need to retire the spreadsheet. Whichever way you go, the existing process has to actually be replaced, not run alongside the new tool indefinitely. The retailers who run the spreadsheet and the new tool in parallel for "a few months" are still running both two years later, and have neither time-to-value nor change.

Where Retailgrid Sits in This Decision

We're transparent about where we land in the framework. Retailgrid is the "buy from people who build with AI" option for retail pricing and assortment. We sit on the side of the table where vendor-side AI leverage compounds — every retailer using the platform pays back work that benefits the next retailer.

That doesn't mean we argue against build categorically. We've watched mid-market retailers build successfully when they had a genuine differentiator, an engineering organization to support it, and first-party data the rest of the market couldn't access. When those three conditions are absent, we'd rather you spend the engineering cycles on whatever your customers will actually pay you more for, and trust the pricing problem to a system that's already 80% done.

The honest answer to "build with AI or buy from people who build with AI" in 2026 is: it depends on which side compounds faster for your business. For most mid-market retailers running 10k–200k SKUs, that math points at buy. For a well-funded specialist with a genuine differentiator, it points at build. The teams that get this decision wrong almost always get it wrong by underestimating year-two TCO of the build path — or by treating hygiene capabilities as if they were strategic differentiators.

Run the five-question audit before you scope the project. Whatever the answer is, run it with eyes open.

Want a deeper read on where AI in retail pricing actually pays off — and where it doesn't? Read our practitioner playbook on AI in retail pricing, or browse the Retailgrid documentation to see what the "buy" side of this decision looks like in practice.